MarinaKuzminykh/iStock via Getty Images

Introduction

We need to discuss two things:

- Americans are generating more income than ever from their investments, including risk-free government debt.

- Once that party ends, money needs to go somewhere.

Starting with the first item, a few weeks ago, The Wall Street Journal reported that “Americans Have More Investment Income Than Ever Before.“

In the first quarter of this year, Americans earned $3.7 trillion from interest and dividends on an annualized basis. That’s up $770 billion from four years ago.

The main driver is elevated interest rates, which allows Americans to generate much higher income – with significantly less risk.

After all, many Americans who have been saving and investing for decades are now able to put their money into money market funds that yield more than 5%, allowing them to generate income with a much more favorable risk profile.

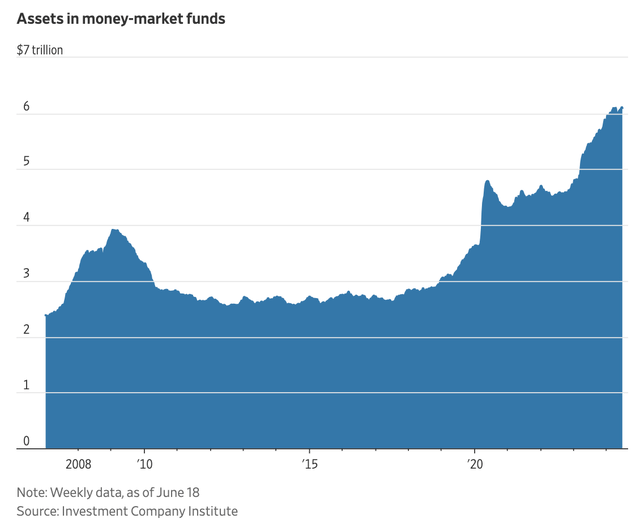

This has pushed assets in money market funds to more than $6.1 trillion, more than twice the numbers we saw five years ago. In fact, over the past two years alone, money market funds attracted more than $2.3 trillion!

The Wall Street Journal

The impact on the spending power of the “haves” (the “have-nots” are a different story) is so big that it actually hurts the Fed’s ability to reduce inflation.

The historic gains aren’t without a potential downside. Americans’ resulting ability to shell out more for goods and services “is going to make it harder for the Federal Reserve to reach their inflation target,” said James Marple, a senior economist at TD Bank. – The Wall Street Journal

With that said, point two is about the potential end of this trend and what this may mean for money flows.

The following quote from a Wall Street Journal article titled “Americans Chasing High Interest Rates Risk Falling Into a ‘Cash Trap’ perfectly shows the impact of the current rate tailwind on spending and what might happen when the Fed starts to cut rates:

The 66-year-old retired banker and his wife have about 60% of their nonretirement assets in Treasury bills and money-market funds that are paying yields of around 5%. With plans to buy a second home in a warmer area, they expect to keep it there until the Federal Reserve cuts short-term interest rates to 4% or below. – The Wall Street Journal (emphasis added)

While it remains to be seen when the Fed will cut rates, it’s a matter of “when” instead of “if.”

That said, rotating money from one asset to another is tough. The same article I just quoted noted that even investment pros struggle with this, as so many factors are an issue, including a person’s age, savings, and financial needs.

So, please don’t see this as personal advice (which I’m not allowed to give anyway) but as food for thought.

For example:

- Elevated rates are fun for income. However, they offer very limited – if any – protection against inflation. People often make the mistake of comparing inflation (which is a rate of change) to yields. A fair comparison would be to compare inflation to dividend growth. Personally, I prefer to own a stock with a 3% yield and with 7% annual growth over a 5% yield bond.

- In a scenario where rates normalize, investors in need of income will have to shift cash to higher-risk investments.

That’s why I’m writing this article.

I will provide four stocks that come with income and income growth. While none of them have a risk profile similar to risk-free bonds (that almost goes without saying), I like the long-term risk/reward and would likely own all of them if I had an income-focused portfolio.

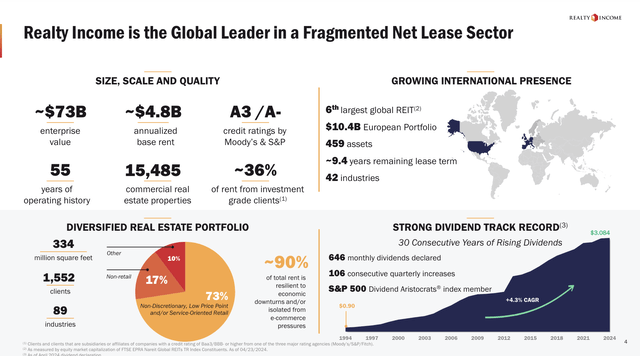

Realty Income (O) – The Monthly Dividend Company With 6% Yield

I’m going to keep this very short, as Realty Income is one of the most discussed stocks on Seeking Alpha. I’ve also covered it in many articles, including co-produced articles with Brad Thomas.

Realty Income is boring, but it’s the right kind of boring.

Yielding 6%, Realty Income has hiked its dividend for 30 consecutive years with a CAGR of 4.3%. It has a credit rating of A- and owns roughly 15,500 properties with low-risk tenants operating in mostly anti-cyclical sectors.

Realty Income

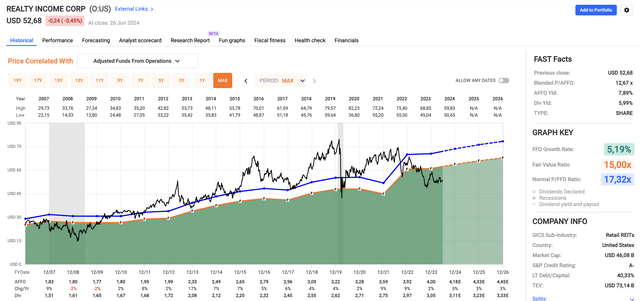

Trading at a blended P/AFFO (adjusted funds from operations) ratio of 12.7x, the company trades a mile below its normalized P/AFFO ratio of 17.3x. On top of that, analysts expect consistent per-share AFFO growth to last, with 3-5% annual growth through 2026.

FAST Graphs

I believe O offers an attractive, low-risk dividend, which will likely result in elevated capital gains the moment lower rates push money from bonds to equities.

That’s when I expect Realty Income to enjoy a much higher AFFO multiple.

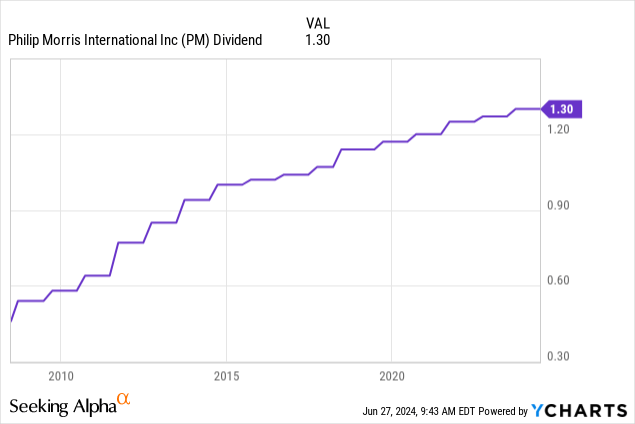

Philip Morris International (PM) – 5% Yield And A Future Without Smoke

On June 21, I wrote an in-depth article discussing the former spin-off from Altria (MO).

Although I’m not necessarily a fan of investing in tobacco, the company has mastered the art of growing in an environment of consistent pressure on its “traditional” tobacco products.

Not only does Philip Morris own five of the top 15 international cigarette brands (two of the top three!), but it also benefits from its international focus, which includes emerging markets with much better growth profiles than developed markets like the United States and Western Europe.

Philip Morris International

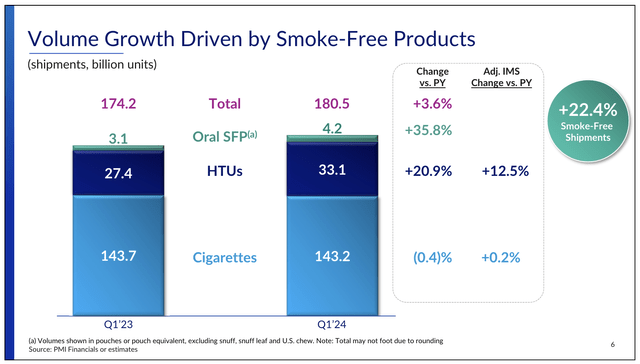

When adding its successful expansion in the smoke-free category, we get a company with highly favorable growth rates.

In 1Q24, it saw a 22.4% growth rate in smoke-free products, supported by stable volumes of cigarettes.

Philip Morris International

Philip Morris is also highly successful in growing the market share of its non-smoke products, as I wrote in my latest PM article:

According to PMI, the IQOS product line showed impressive progress, with a 13% increase in adjusted in-market sales volumes and a 21% rise in total shipments.

Meanwhile, the new IQOS ILUMA device has been key in this success as well, as it is now available in 64 markets and represents roughly 100% of IQOS volumes outside of Russia.

ZYN volumes were up 80% in the United States. This product holds a 74.3% category volume market share and a 79.3% retail volume share.

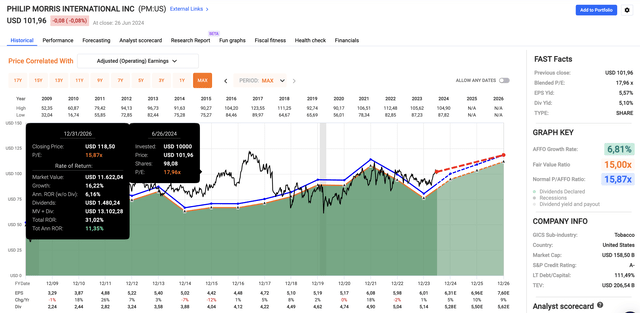

On top of that, the company has a credit rating of A- and is expected to generate more than $10 billion in free cash flow this year. Through 2026, that number could rise to $11.5 billion, implying a 7.3% free cash flow yield.

These numbers protect the company’s 5% dividend yield, which comes with a five-year CAGR of 2.7%.

While 2.7% average annual dividend growth isn’t exciting, the future is looking bright, as analysts expect 5% EPS growth this year, potentially followed by 10% and 9% growth in 2025 and 2026, respectively.

When adding its 5% yield and the assumption that PM will continue to trade at its normalized P/E ratio of 15.9x, we get a favorable (theoretical) annual return outlook of 11-12%.

FAST Graphs

The next one is a financial giant.

CME Group (CME) – 5%-ish Yield With Special Dividends And A Great Valuation

CME Group is one of my all-time favorite financial dividend growth stocks. However, it’s also a stock that is currently being pressured by fears of new competition.

My most recent in-depth article on this company was written on May 25, when I called it “One Of My Best Ideas In Finance” in the title.

CME Group is a transaction-based company, meaning it makes money whenever people use futures and options on one of its many exchanges.

- CME (Chicago Mercantile Exchange) offers a diverse range of futures and options contracts, including interest rates, equity indices, foreign exchange, agricultural commodities, and more.

- CBOT (Chicago Board of Trade) trades futures and options contracts for agricultural products, interest rates, and equity indices.

- NYMEX (New York Mercantile Exchange) specializes in energy and metals trading, including contracts for crude oil, natural gas, and various metals like gold and silver.

- COMEX (Commodity Exchange, Inc.) focuses on metal products, offering contracts for gold, silver, copper, and other base metals.

The company’s products include some of the world’s most traded futures and options, including NYMEX WTI crude oil, NYMEX Henry Hub, COMEX silver/gold/copper, CBOT corn, and the famous S&P 500 e-mini contract.

Even better, the company has a wide-moat advantage, as it has exclusive license agreements for futures on the S&P 500, which is part of a bigger portfolio of exclusive rights.

I added emphasis to the quote below:

In 2010, CME Group acquired a majority stake in Dow Jones Indexes, which was combined with S&P’s index business in 2012 to form S&P Dow Jones Indices LLC, of which CME Group now has a 27% ownership stake. S&P Dow Jones Indices LLC combines the world class capabilities of the S&P and Dow Jones Indices, and is a significant player in passive investing, including the exchange-traded fund (ETF) industry value chain. As part of the joint venture, we acquired a long-term, ownership-linked, exclusive license to list futures and options based on the S&P 500 Index and certain other S&P indices. – CME 2023 10-K

That said, while CME has outperformed the S&P 500 by a wide margin over the past ten years, current stock price weakness is caused by fears of new competitors.

On June 21, JPMorgan downgraded CME Group due to the launch of FMX, which is a futures exchange backed by major banks – including JPMorgan.

Hence, I’m not a huge fan of using JPMorgan’s quotes, as I sense a slight conflict of interest – to put it mildly.

However, I’m doing it anyway:

“While all that have tried to compete with CME (CME) have failed, we see FMX having the most compelling offering to date, supported by state-of-the-art technology, powerful partners, and a compelling value proposition including lower commission and competitive, if not potentially better, portfolio margining,” he noted. – Via Seeking Alpha

Please note that this will only apply to interest-rate trading.

Although I don’t like this news, I am not worried. CME Group has a wide moat that will be hard to penetrate. New exchanges will have to prove they are capable of delivering similar results. So far, many have tried, but none have achieved it.

It also helps that CME isn’t standing still. The company is further expanding its relationship with Alphabet’s (GOOGL) Google to develop cloud and colocation facilities.

Google also has a $1 billion equity investment in CME Group and seems to be very eager to build a very powerful platform:

Firms that migrate trading to the new facility will also have access to Google’s cloud services including artificial intelligence tools and data analytics, CME and Google said. The matching engine, which links buyers and sellers in a trade, will move to the cloud. – Bloomberg

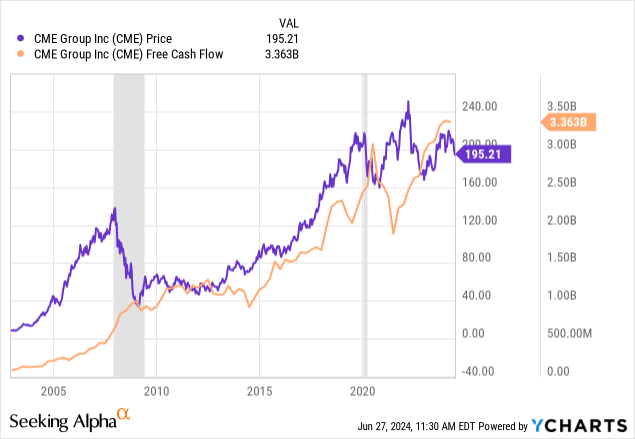

On top of that, it’s a company that consistently returns 100% of its free cash flow to shareholders, using four regular quarterly dividends and one special dividend, often announced in the fourth quarter.

CME Group

At current prices, the company has an implied free cash flow yield of 5.5% for 2024 ($3.9 billion 2024E FCF), which leads me to believe that this will be the total annualized yield investors will enjoy when buying at current prices.

It also helps that the company’s income is often very strong during recessions. While CME stock tends to sell off when the market tanks, elevated volatility is a huge tailwind.

On top of that, I believe CME is one of the cheapest high-yield stocks on the market.

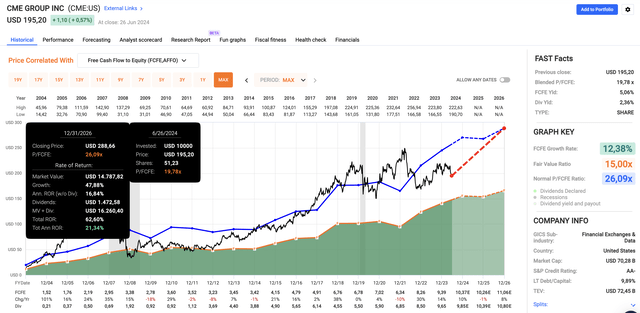

As the company has a cash conversion rate of more than 100%, I use FCFE to value CME. FCFE is free cash flow to equity.

Currently, CME trades at a blended P/FCFE ratio of 19.8x, which is below its normalized FCFE ratio of 26.1x.

FAST Graphs

Using the FactSet data in the chart above, CME is expected to grow per-share FCFE to $11.06 by 2026. This gives the company a fair stock price of roughly $290, almost 50% above the current price.

In my most recent in-depth article, I used a P/E ratio approach, which resulted in a $278 price target.

While CME won’t likely reach this target in the months ahead, I believe we are dealing with a highly favorable long-term investment that comes with both income and growth.

And before I forget to mention it, CME has a credit rating of AA-, one of the best ratings in the world.

Kinder Morgan (KMI) – 6% Midstream Income

Kinder Morgan is sometimes a bit of a sensitive topic, as some investors have had a bad experience with the company in the past.

The company has been through two major sell-offs in 2015 and 2020 – including a dividend cut.

However, currently, it is performing well and has become one of my favorite midstream companies.

My most recent article on this company, which does NOT issue a K-1 form, was written on March 28, when I wrote the following:

With its extensive network and strategic positioning in major basins, Kinder Morgan stands out as a reliable income generator with an elevated dividend yield and a promising growth outlook.

Trading almost 30% below its fair stock price, I believe KMI offers tremendous value for a wide range of dividend investors.

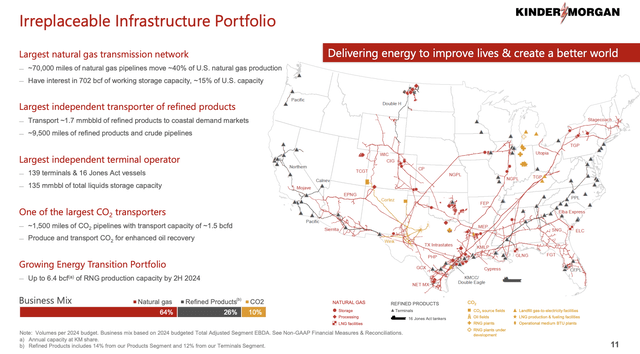

One major benefit here is its size. Kinder Morgan has a network of roughly 70,000 miles of natural gas pipelines. This network moves 40% of US natural gas production!

It also has an interest in more than 700 billion cubic feet of storage, which equals 15% of US storage capacity.

Kinder Morgan

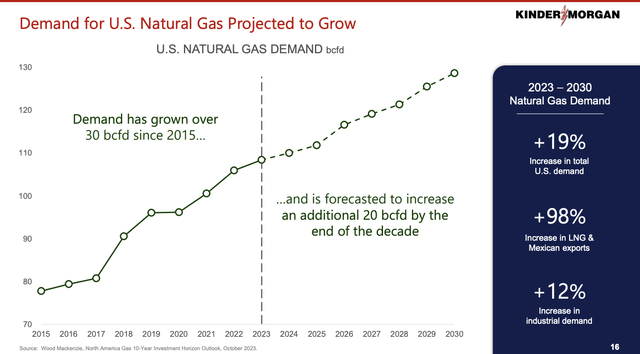

Natural gas is a great place to be, as demand is expected to see unprecedented growth, fueled by LNG exports and rising AI-related electricity demand growth.

Total demand is expected to rise by 19% through 2030, with a doubling in LNG exports. Even industrial demand is expected to rise by 12%.

Kinder Morgan

This bodes well for KMI, as 27% of its contracts are fee-based, where the company is paid on throughput. 68% of its contracts are take-or-pay, where it makes money regardless of throughput.

Furthermore, this business model comes with a load of cash. Next year, KMI is expected to generate $3.4 billion in free cash flow, 7.8% of its market cap.

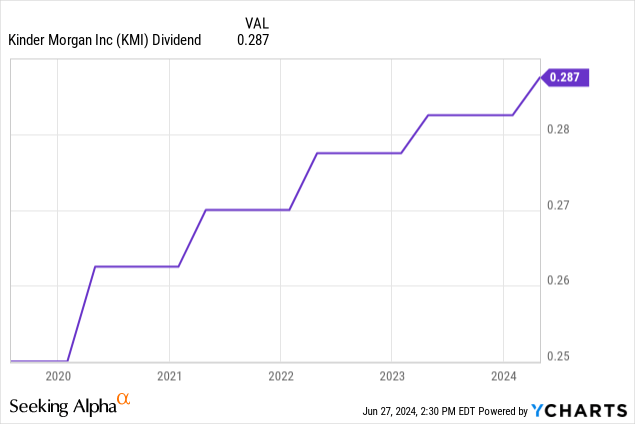

An FCF yield of almost 8% protects the company’s 5.8% dividend yield, which has a five-year CAGR of 6%.

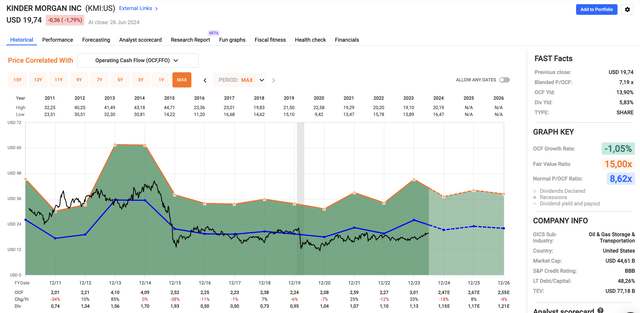

Valuation-wise, KMI trades at a blended P/OCF (operating cash flow) multiple of 7.2x. This is below its long-term normalized OCF multiple of 8.6x, which I consider to be fair.

FAST Graphs

Based on $2.55 in 2026E per-share OCF, we get a fair stock price of $22, 12% above the current price.

Including its 6% yield, we are likely dealing with a company capable of consistent double-digit annual returns.

Takeaway

Americans are enjoying unprecedented investment income, mainly due to high interest rates driving gains in money market funds and Treasury bills.

However, this benefit is likely temporary and poses a challenge to the Fed’s inflation goals.

Hence, as rates inevitably decline over time, investors must pivot to higher-risk assets to sustain income.

To address this, I’ve highlighted four impressive stocks offering reliable dividends and growth potential:

- Realty Income: With a 6% yield and a history of steady dividend hikes, this stock is a cornerstone for income-focused portfolios.

- Philip Morris International: Despite the tobacco industry’s challenges, PM’s smoke-free products and international market expansion promise growth and a secure 5% yield.

- CME Group: A resilient financial giant offering special dividends and a strong growth outlook, even in light of competitive pressures.

- Kinder Morgan: A leader in natural gas infrastructure with a 6% yield, benefiting from rising energy demand.

I believe these picks provide a balanced approach to income and growth for the years ahead.